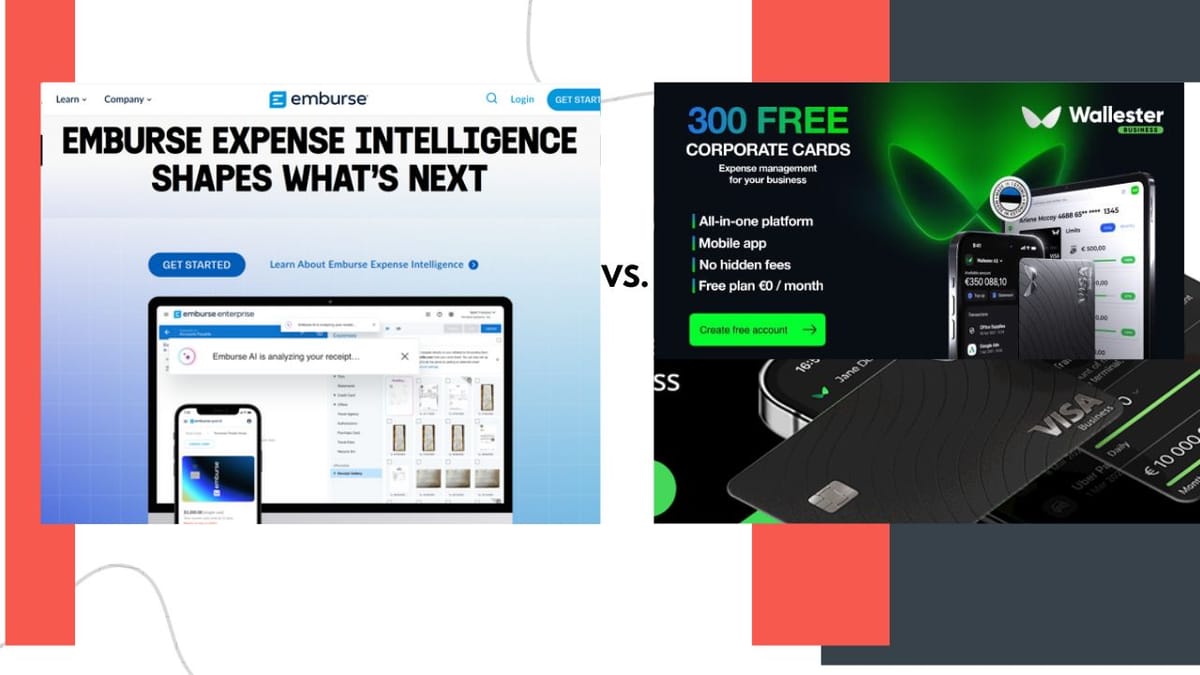

Cost or Control? The Definitive Guide to Choosing Between Wallester and Emburse

Choosing between Wallester and Emburse depends on one thing: cost versus control. Wallester offers the lowest TCO and highest card volume (including 300 free virtual cards), while, Emburse provides proactive, AI-driven policy enforcement and global compliance

The Core Axis of Comparison: Cost-Efficiency & Volume vs. Proactive Compliance & AI Sophistication

Corporate finance isn’t just about chasing receipts anymore. Today’s expense management platforms need to catch policy violations before they happen, keep a close eye on SaaS spending, and deliver real-time compliance no matter where your teams are.

When it’s time to pick a platform, it really comes down to what matters most to your business. If you want to drive down the cost of each virtual card and ramp up how many you issue, Wallester is the way to go.

This E-E-A-T-driven review provides an exhaustive analysis, separating the technical capabilities, fee structures, and specific use cases for Wallester and Emburse. We detail how one dominates the high-volume, low-cost virtual card market, while the other provides a premium, finance-first AI infrastructure essential for mid-market and global enterprises.

Wallester: The Free Frontier of High-Volume Virtual Card Issuance

Wallester positions itself as the accessible and multi-functional solution for companies prioritizing cost control and high-volume card creation. Its core appeal lies in its extremely low friction to entry and its ability to solve specific pain points related to digital advertising and "Shadow IT" spending.

1.1 The Dominance of the FREE Pricing Structure (Cost-Efficiency)

Wallester’s strategic advantage is its highly compelling entry-level pricing. They offer a FREE edition priced at €0 per month, which is designed to capture market share from startups, agencies, and e-commerce businesses that rely heavily on segregated card spending but have strict budget limitations.

Key Financial Inclusions in the FREE Tier:

- 300 Free Virtual Cards per Month: This massive allowance is unparalleled in the expense management space and instantly positions Wallester as the superior choice for managing diverse digital ad spend across platforms (Google, Facebook, TikTok) or for managing individual SaaS subscriptions.

- Unlimited Physical Card Issuance: This allows companies to equip their entire team with physical cards without incurring additional user or card fees, a common cost-inflator at many competing platforms.

- Unlimited Users: Crucially, Wallester does not base its core pricing on the number of active users, removing the single largest scaling cost associated with traditional expense software.

For companies requiring higher transaction limits and card volumes, Wallester’s paid tiers (starting typically around €199/month for the basic Business package) scale up substantially. The Platinum tier, for example, can include up to 18,000 virtual cards, resulting in a cost as low as approximately €0.056 per card per month. This scale is ideal for large media buying operations or global e-commerce companies that require localized virtual cards for fraud minimization and targeted spending.

1.2 Strategic Use Case: Taking Control of "Shadow IT" and SaaS Spending

Wallester Business doesn’t just offer virtual cards for payments; it turns them into a built-in system for controlling your company’s software costs. Today, “Shadow IT” is a real headache. Employees sign up for SaaS tools on their own. Some subscriptions get forgotten, some barely see any use, and the company keeps paying the bill.

Here’s how Wallester keeps things under control:

- One card per subscription: Every software tool gets its own virtual card. Slack? That’s its own card. Zoom? Another one. Adobe? Same thing. You won’t have to deal with messy expenses or weird charges showing up on your statement anymore.

- Real-time limits and alerts: Set a monthly cap for each card, like $50 for Slack. If you hit that limit, Wallester lets you know immediately. This ensure you stay on top of your spending without nasty surprises.

- Automatic cancellation: When someone leaves the team or a project wraps up, you can freeze or cancel just the card tied to that subscription. Everything else keeps running smoothly.

All this cuts down on wasted money from old, forgotten subscriptions. The finance team gets a clear, up-to-the-minute view of every recurring software expense, so you can actually stay ahead of costs instead of chasing them later.

This capability significantly reduces waste from forgotten recurring subscriptions and provides the finance team with a granular, real-time audit of all recurring software expenses, thereby establishing a proactive cost governance model.

Wallester Business takes virtual cards way beyond just making payments—they become your built-in system for managing costs. These days, one of the biggest financial headaches for companies is "Shadow IT." Basically, employees sign up for all kinds of SaaS tools on their own. Some get forgotten, others never get used, and the bills just keep adding up.

1.3 Operational Experience: The Performance Caveat

While the pricing and volume capabilities are industry-leading, a balanced E-E-A-T analysis must incorporate real-world user feedback regarding operational performance. Verified user reports often cite challenges related to operational speed:

- Slow Desktop Performance: The desktop version of the Wallester management portal can occasionally experience "slow performance" during peak usage times, which may create friction for finance teams processing high volumes of reconciliations simultaneously.

- Card Issuance Delays: While the ability to issue cards is free and high-volume, some users report occasional delays in the instantaneous deployment of both physical and virtual cards compared to competitors who prioritize immediate issuance.

This caveat confirms that while Wallester is the clear financial winner for budget and volume, businesses where instantaneous card deployment and system responsiveness are paramount may encounter occasional minor operational friction.

2. Emburse: Finance-First AI with Real-Time Compliance

Emburse, on the other hand, takes a different approach. It's built for mid-sized and global companies that care most about being audit-ready, enforcing policies upfront, and handling the headaches of international tax and currency. Emburse charges a premium, but it backs that up with its own finance-focused AI tech.

2.1 Emburse AI’s Core Function: Proactive Policy Enforcement

What really sets Emburse apart is its custom-built AI. Instead of just chasing receipts after the fact, Emburse flips the script. It makes compliance proactive.

Here’s what that looks like:

- Pre-Submission Policy Enforcement: Most systems only flag issues after you’ve already submitted an expense report. Emburse flips that around. Its AI steps in right when you’re about to spend. If you try to buy something outside company policy or go over your limit, Emburse sends you an alert or just blocks the purchase instantly. It stops problems before they even start.

- Advanced Receipt OCR and Categorization: Emburse’s AI uses optical character recognition and machine learning to pull details off your receipts—merchant name, date, amount, all of it. Then it checks those details against your card data and automatically files the expense into one of 39+ categories. So finance teams do less manual work, and there’s a lot less room for error.

- Automated Audit Trails: Emburse’s AI keeps an eye out for anything unusual—potential fraud, odd patterns, you name it. Every expense gets a complete, tamper-proof audit trail. For companies under strict regulations, this kind of documentation is essential.

Having this kind of control, where you can actually stop non-compliant spending before it happens, pays off for companies. Especially those that deal with high audit risks or have trouble keeping everyone in line with policy as they grow.

Emburse’s core differentiator is its purpose-built artificial intelligence, which shifts expense management from a reactive, receipt-chasing process to a proactive system of compliance.

2.2 Global Readiness and Multi-Jurisdictional Compliance

For organizations with international operations, Emburse provides a specialized infrastructure that Wallester’s current model cannot easily match.

Global Localization Features:

- 100+ Countries Supported: Emburse works in more than 100 countries. The platform isn’t just available—it actually speaks the language of local business. You get support for regional payment standards, tax laws, and currency formats, so your finance team doesn’t have to scramble to keep up with every new market.

- Global VAT and Tax Reconciliation: Handling VAT and other international taxes is usually a headache for global companies. Emburse tackles that directly. It handles multi-currency transactions and automates VAT reconciliation, taking much of the pain out of recovering foreign taxes. You don’t have to worry whether your reporting meets local rules—it does.

- Historical Credibility: The company’s no stranger to innovation, either. Emburse was the first to launch an expense reporting app on the Apple App Store. That’s not just trivia—it shows they know how to build reliable, scalable mobile tech that keeps up with global business.

Emburse isn’t new to this, either. They’ve been ahead of the curve for a while—actually, they were the first to launch an expense reporting app on the Apple App Store. That kind of track record shows they know how to build reliable, mobile-friendly expense tech that works on a global scale.

2.3 Pricing Structure: A Tiered Approach to Sophistication

Emburse uses a tiered, quote-based pricing system. You get what you pay for, with each level unlocking more advanced features and dedicated compliance support. This structure matches the needs of organizations looking for robust, high-value solutions.

3. Comprehensive Comparative Analysis: TCO, Integrations, and Scalability

The decision between Wallester and Emburse requires a granular look at the Total Cost of Ownership (TCO) relative to the specific business functions needed.

3.1 Total Cost of Ownership (TCO) Analysis

TCO must account for both subscription fees and the opportunity cost of non-compliance or poor cash flow management.

Financial Metric | Wallester (Cost/Volume Focus) | Emburse (Compliance/AI Focus) | Strategic Implication |

|---|---|---|---|

Subscription Base | Starts at €0/month (FREE tier) | Tiered, Quote-based (Higher monthly cost per user) | Wallester minimizes fixed costs; Emburse reflects value in sophisticated software. |

Cost Per Virtual Card | Extremely low (€0.00 – €0.056) | Variable, typically higher than Wallester | Wallester is unbeatable for high-volume advertising/SaaS spend. |

Audit Risk Mitigation | Standard tracking and limits | High. Proactive AI enforcement significantly lowers risk of policy violations. | Emburse’s ROI comes from reducing costly audit and compliance failures. |

Global Fee/FX Complexity | Requires external management/tracking | Integrated multi-currency, VAT reconciliation, and localization features. | Emburse is essential for frequent international travel/spending. |

The TCO Verdict: So, let’s break down what the TCO actually means here. If you’re running a local business and just need to churn out a bunch of virtual cards to keep spending organized, Wallester wins on price, plain and simple.

But if your company’s bigger, or you’re dealing with international operations, Emburse comes out on top. It covers those sneaky costs that add up fast, like compliance issues, sorting out expenses by hand, and messy tax stuff in different countries.

3.2 Implementation, Integration, and Data Flow

Both platforms work smoothly with the major accounting software. You’ll get solid integrations no matter which one you choose. But when it’s time to actually roll things out, the differences start to show.

Aspect | Wallester Business | Emburse | Comparison Point |

|---|---|---|---|

Integration Philosophy | Open API-focused for custom data flow. | Deep, pre-built, two-way sync with major ERPs (NetSuite, SAP, etc.) and accounting platforms (QuickBooks, Xero). | Emburse offers better out-of-the-box depth for complex ERPs. Wallester better for developers needing custom connection layers. |

Receipt Capture | Reliable OCR and categorization. | Advanced, finance-first AI OCR with real-time policy checks. | Emburse’s AI provides better data validation before the expense is categorized. |

Speed of Implementation | Generally faster setup due to simpler feature set. | Longer setup time required to customize and deploy complex, policy-driven AI rulesets. | Wallester is quicker to deploy for immediate needs. |

3.3 Scalability and Future-Proofing

- Wallester’s Scaling Path: Wallester scales horizontally, primarily via card volume. It is future-proofed by its Open Developer API, which allows large organizations to integrate the card issuance engine directly into their proprietary financial software or enterprise resource planning (ERP) systems. This is ideal for companies that need a custom-built solution that leverages a high-volume card provider.

- Emburse’s Scaling Path: Emburse scales vertically through feature sophistication. As a business grows from mid-market to enterprise, its need for global localization, complex compliance controls (e.g., regional spending caps, specific per-diem rules, and complex reimbursement workflows) increases. Emburse’s unified platform—covering expense, travel, invoice, AP, and payments—is designed to handle this vertical growth without requiring a platform switch.

4. Security, Fraud Prevention, and E-E-A-T Compliance

Financial integrity is very important: both platforms utilize core security standards; however, Emburse’s AI provides a layer of proactive protection focused on reducing internal risk.

4.1 Data Protection and Encryption

Both providers prioritize fundamental security mandates to ensure:

- Bank-Level Encryption: Data are transferred using secured Transport Layer Security (TLS) and stored with industry-standard encryption (e.g., AES 256-bit).

- PCI Compliance: They maintain strict adherence to PCI Data Security Standards (DSS) for all cardholder data, ensuring that payment details are handled securely.

4.2 The Crucial Difference between Proactive vs. Reactive Fraud Detection

- Wallester: Wallester: Primarily focused on using standard rules-based systems for fraud detection (e.g., locking cards after a certain number of failed transactions, blocking purchases in high-risk geographies). Its main security benefit lies in segregation; if one virtual card is compromised, only the funds on that card are at risk, not the entire company budget.

- Emburse: Leverages its finance-first AI for continuous pattern-based monitoring. The AI actively looks for signs of policy drift, unusual spending velocity, and irregular expense patterns that might indicate internal fraud or external compromise. This proactive, behaviour-based fraud detection goes beyond simple rules and provides a superior layer of risk mitigation.

4.3 Regulatory Oversight and Audit Readiness

To establish authoritativeness and Trust, a high level of compliance is key:

- Emburse's entire philosophy is built around audit readiness, with the AI ensuring every step, from receipt capture to policy, cheque is logged and verified in real time. This level of granular control is essential for public companies

- Wallester, on the other hand, provides reliable expense tracking and management, but its primary focus remains on the card issuance and API utility rather than deeply complex policy validation or multi-jurisdictional tax law.

5. Final Verdict and Strategic Recommendation Matrix

The choice between Wallester and Emburse is a strategic decision that depends entirely on a company’s volume, budget, and regulatory profile.

Parameter | Wallester (Recommended) | Emburse (Recommended) |

|---|---|---|

Best For | Startups, E-commerce, Marketing Agencies, Businesses with High SaaS Spend. | Mid-Market, Global Enterprises, Highly Regulated Industries (e.g., Financial Services). |

Primary Goal | Minimizing Cost and maximizing virtual card creation volume. | Maximizing Compliance and automating policy enforcement globally. |

Key Differentiator | €0/month FREE Tier with 300 virtual cards and Open API. | Finance-First AI for proactive, real-time policy enforcement and global VAT tracking. |

Key Caveat | Occasional reported friction with desktop speed and card deployment delays. | Higher cost structure; requires more involved setup for complex AI policy customization. |

Recommendation:

- If your budget is tight and you need hundreds of virtual cards primarily for digital marketing, SaaS subscriptions, or segregating vendor payments, Wallester provides the best financial ROI and card volume scalability. → Start with Wallester's FREE Virtual Card Edition

- If you have complex policy rules, require global support across 100+ countries, or operate in an industry where audit risk is high and pre-submission compliance is non-negotiable, Emburse is the necessary investment for sophisticated control and AI-powered risk mitigation. → Request a Custom Demo for Emburse AI Compliance

This analysis confirms that both platforms are best-in-class within their respective niches, making the final decision a function of your specific business maturity and financial control needs.